1) Global Financial Impacts

- Increase in Claims: Insurance companies are going to experience an increase in claims. In fact, numerous claims are already occurring in some specialized branches, such as health, travel or loss of profits, and could continue in other areas such as cyber attacks or credit insurance.

- Economic slowdown: The more general concern is how the outbreak could affect the economic environment, specifically the growth prospects and profitability of insurers' underwriting and investment portfolios.

- Investments: The fall suffered by all the world's stock markets has had a great impact on the valuation of portfolios. Although it is true that debt constitutes a very significant part of their assets, mainly in life companies, the collapse of equities will have a very significant impact on the sector. In the following graph, the Insurance Industry is seen as one of the most affected sectors in its market capitalization.

Impact on Market Capitalization by Sector as of March 25, 2020

%2010.39.38.png?width=2402&name=Captura%20de%20Pantalla%202020-04-07%20a%20la(s)%2010.39.38.png)

2) Impacts by type of coverage and risk

Some negative impacts are related to the coverage of contingencies to which companies operating mainly in the health and life branches may be obliged. However, there are other examples of greater losses in coverage related to: cancellation of events, travel insurance, insurance that covers the interruption/delay of basic supplies for certain industries, health insurance or credit insurance or in reinsurance.

It is also highly probable that, as a result of the interruption of normal activity, in the short term there will be a reduction in claims in other areas where insurance has a significant weight, for example, car insurance and insurance related to mobility.

The individual impact in each case will depend on the products marketed, the coverage offered and, ultimately, any exclusions in the drafting of policies for losses attributable to the effects of epidemics or pandemics.

- Health insurance: policyholders are concerned about whether or not health care will be covered by insurance in the event of symptoms of possible infection, as well as coverage for treatment.

- Travel insurance: another concern expressed by policyholders is whether travel cancellation due to coronavirus will be possible and what happens to reimbursements.

- Civil liability insurance: both companies and managers are concerned about the responsibilities they may assume if measures to prevent the disease have not been taken or if any action or inaction considered contrary to the duty of due diligence of the administrators has been carried out.

- Credit insurance: companies analyse the possible non-payment of their suppliers and the coverage provided by their credit insurance.

- Personal insurance: Insured parties consider whether compensation should be paid in the event of death or temporary or permanent disability or major disablement due to the coronavirus.

Payment protection insurance: with regard to payment protection, policyholders consider the impact of temporary work incapacity, unemployment and possible non-payment of loan instalments not linked to mortgage products.

Insurance in cyber security: companies expect to suffer cyber attacks, taking into account that the networks used for "teleworking" are domestic and not professional.

Source: https://www2.deloitte.com/es/es/pages/legal/articles/impacto-del-covid-19-en-el-sector-seguros.html

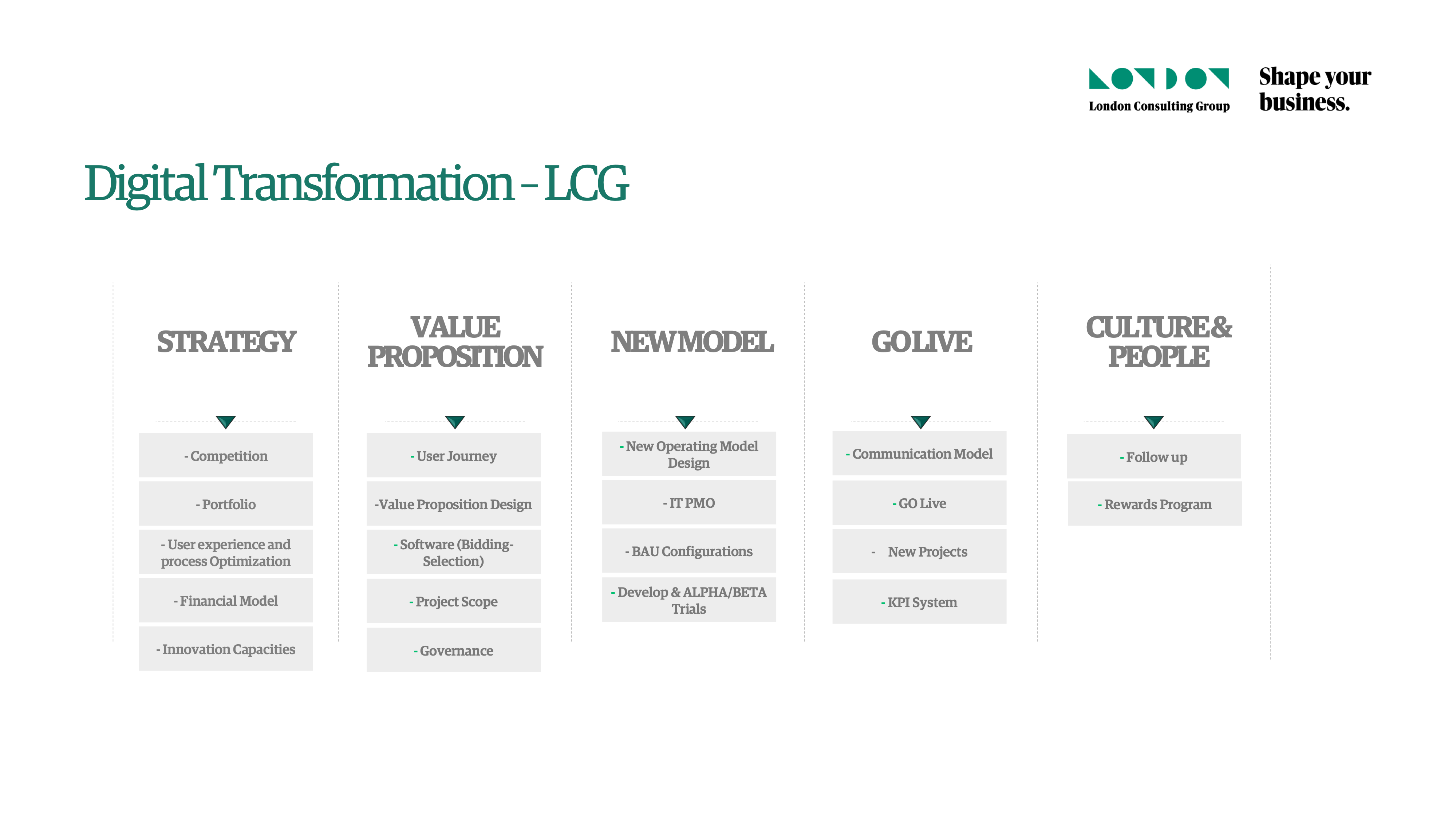

3) Digital Operation

The Covid-19 can also interrupt the customer service of an insurance company, starting with its distributors. Agents, brokers and financial advisors are likely to face many of the same logistical and risk management challenges as their insurers, especially since many may also have to work from home.

Operating through digital media is of great importance in these times of confinement, both in the Issuance and Claims processes. To ensure the continuity of the operation, the different actors in the chain need to have processes and platforms for remote transactions: final insured, agents and collaborators of the insurer.

This period should serve as a catalyst for insurers to redefine their strategic and transformation priorities.

There is no single recipe for digital transformation, but different consulting firms have designed methodologies to accompany their clients in the process.

Download our Digital Transformation Methodology

{kind=link}